Trademark Judgement – ME Technology

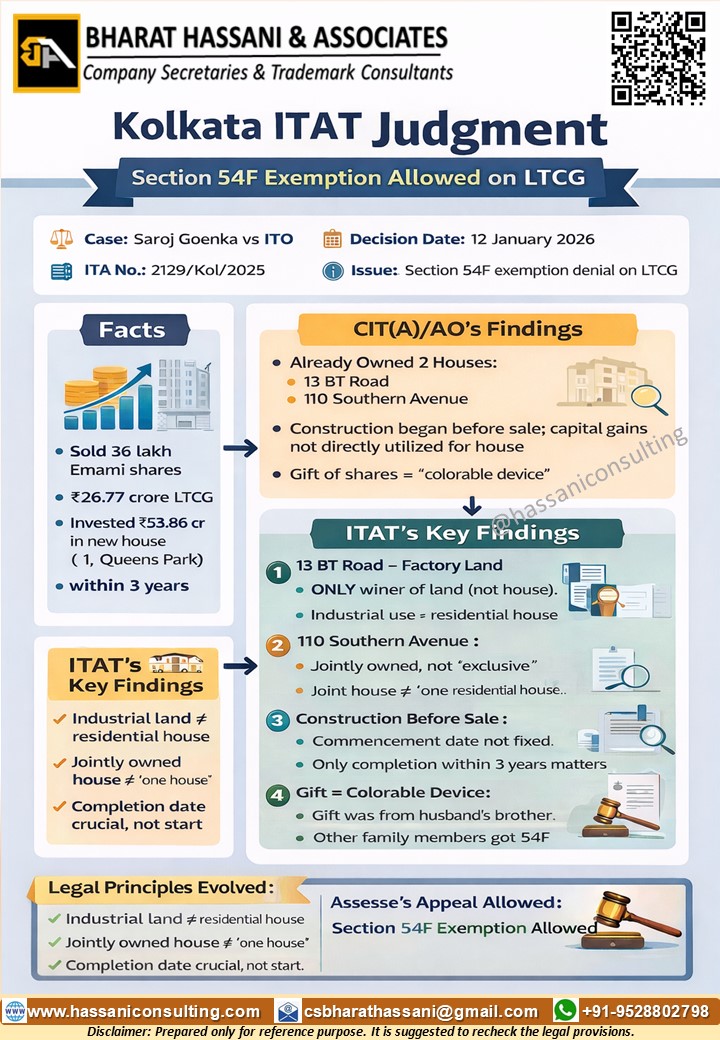

🏛️ Case Brief: Saroj Goenka v. ITO

Income Tax Appellate Tribunal, Kolkata · ITA No. 2129/Kol/2025 · AY 2021–22 · Decision: 12 January 2026

⚖️ Facts of the Case

The assessee Smt. Saroj Goenka sold 36,00,000 shares of Emami Ltd. on 13 July 2020 resulting in Long-Term Capital Gain of ₹26.77 Crore.

The assessee claimed exemption under Section 54F of the Income Tax Act on the ground that the capital gains were invested in the construction of a residential house at 1, Queens Park, Kolkata.

The residential property was completed on 09 June 2022, within the statutory period of three years from the date of transfer.

⚠️ AO / CIT(A) Findings

- Assessee allegedly owned more than one residential property.

- Property at 13 B.T. Road and 110 Southern Avenue considered additional houses.

- Construction of new residential property began before sale of shares.

- Capital gains were allegedly not directly utilised for construction.

- Shares received by gift considered a “colourable device” to claim exemption.

🔍 ITAT Key Findings

- 13 B.T. Road Property: Tribunal held that the assessee owned only the land while the factory building belonged to the tenant. Hence it was not a residential property.

- 110 Southern Avenue: The property was jointly owned with family members. Joint ownership does not amount to owning another residential house for Section 54F.

- Construction Before Sale: Section 54F does not require construction to begin after the sale. Only completion within three years is necessary.

- Utilisation of Capital Gains: Direct use of sale proceeds is not mandatory if equivalent investment is made in the residential property.

- Gift of Shares: Shares were received from the assessee’s husband’s brother. Clubbing provisions were therefore not applicable.

🧾 Final Order

- ITAT set aside the order of the CIT(A).

- Assessing Officer directed to allow exemption under Section 54F.

- The appeal of the assessee was allowed.

💡 Key Legal Takeaways

- Industrial land cannot be treated as a residential house for Section 54F.

- Joint ownership does not disqualify exemption.

- Completion of construction within three years is the key requirement.

- Direct utilisation of sale proceeds is not mandatory.

- Beneficial provisions like Section 54F should be interpreted liberally.

⚖️ Conclusion

The ITAT held that the assessee satisfied all the conditions prescribed under Section 54F of the Income Tax Act. Accordingly, the order of the CIT(A) was set aside and the Assessing Officer was directed to allow the exemption claimed by the assessee.

📢 Share this Case:

Bharat Hassani & Associates (BHA) is an integrated corporate secretarial and legal services firm, offering ONE STOP SOLUTION for all the corporate compliances and legal requirements.